Diversion - CROPPED - credits Filmhuis Den Haag NUREALITY

In recent years, the XR ecosystem has become increasingly professionalized, driven by supportive public policy. Private actors are now investing in the sector, financing studios and dedicated immersive venues. Behind this momentum, several questions remain open: where does immersive money actually come from? Who bears the cost of XR creation in France? Questions that, beneath their apparent simplicity, reveal the full complexity of XR’s economic balance.

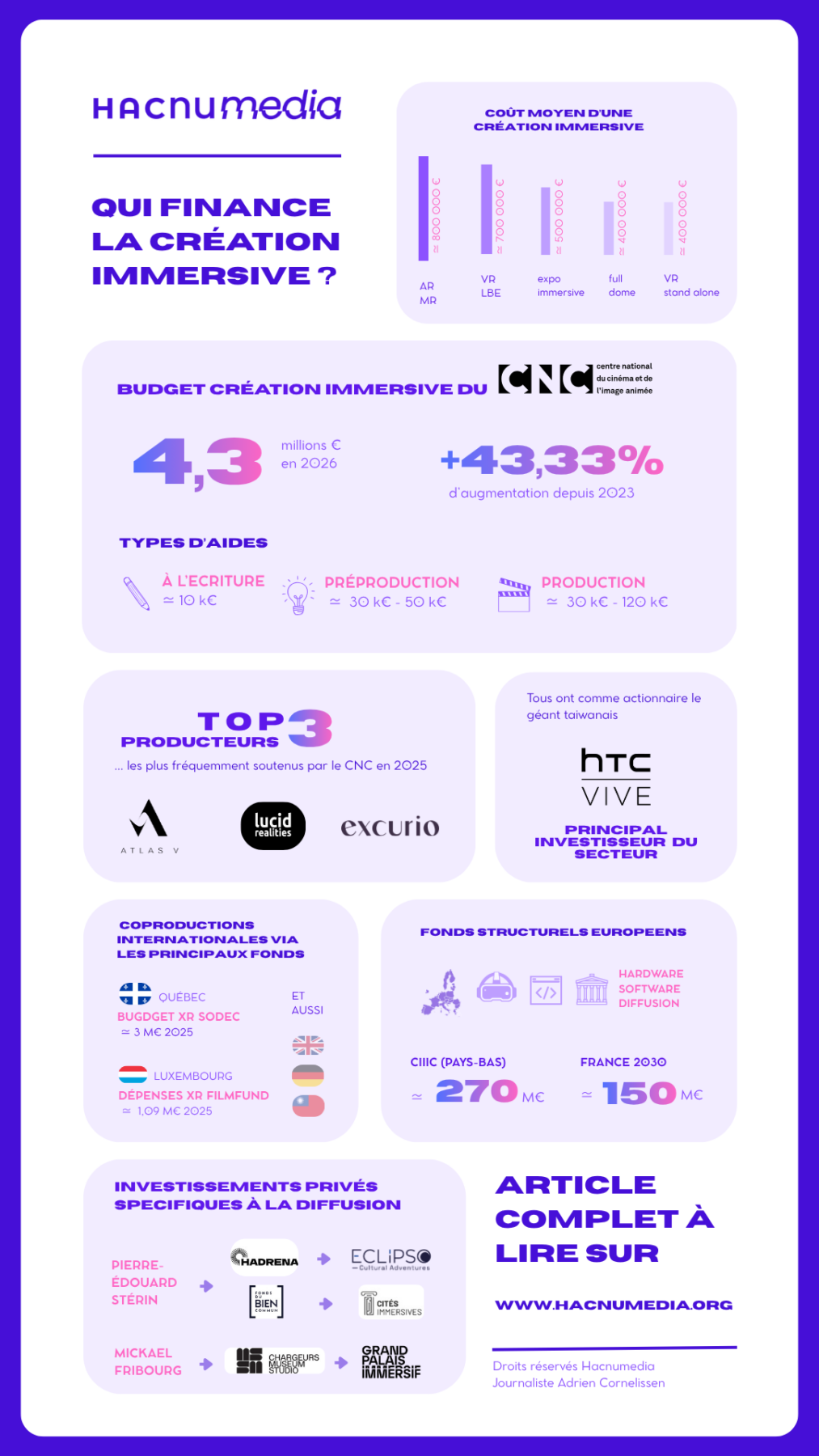

The term XR encompasses a wide range of artistic forms, each corresponding to distinct production realities. At the 2026 edition of iMMERSITY in Angoulême, Olivier Fontenay, Head of Digital Creation at the CNC, outlined a taxonomy of projects along with the average budgets of those that applied for CNC support in 2024 and 2025: augmented or mixed reality works (average budget around €800,000), location-based entertainment (LBE) virtual reality (around €700,000), immersive exhibitions (around €500,000), full-dome projections (around €400,000), and standalone VR works (around €400,000). Installations—based on production and distribution models specific to the digital arts sector—are intentionally excluded from the analysis that follows. These figures immediately raise a key question: who funds these works? A short—and therefore incomplete—answer might fit into three letters: CNC.“If the CNC were to stop supporting immersive creation, everything would come to a halt overnight,”says Mathieu Pradat, producer and founder of La Prairie Productions.. Indeed, for several years now, the French institution historically dedicated to cinema has made immersive creation a priority. To understand why, we need to look back. The first support mechanisms for immersive creation date back to 2014, at a time when projects were still funded through so-called “New Media” channels or through the DICRéAM program, which was more closely aligned with digital arts. Over the years, the “New Media” framework became “Digital Experiences,” before eventually being renamed the “Immersive Creation Fund.”

In budgetary terms, the numbers reflect a clear commitment from the CNC, even if the scale remains modest relative to the CNC as a whole—and to the broader cultural industries. In 2024, the allocated budget was approximately €3 million. In 2025, the immersive fund increased to €4.4 million. For 2026, €4.3 million has already been earmarked. With funding hovering around €4 million for the past two years, could this represent a plateau for the years ahead? Not necessarily, since these amounts remain tied to the CNC’s overall budget and, indirectly, to cinema attendance levels, which determine the institution’s revenue streams. The CNC is then free to arbitrate how resources are distributed among its various funds. In this regard, current CNC president Gaëtan Bruel has demonstrated a strong commitment to immersive creation since taking office in 2025. That commitment has been visible in his international presence, notably at Venice Immersive last year—one of the sector’s flagship events.

Multiple Funding Mechanisms

Concretely, the CNC has structured its support through several production-oriented schemes: writing grants (around €10,000 for authors), pre-production and production funding. These three well-known schemes are complemented by development support and, since January 1st, 2026, by a distribution aid scheme—already existing but now open to online immersive works, which in reality concern only a small portion of XR production, as the market remains largely centered on LBE. In pre-production, funding typically ranges between €30,000 and €50,000 depending on project scope and ambition. In production, however, the scale shifts: grants can range from €30,000 to €120,000. The lower end usually supports experimental artistic proposals led by independent companies often emerging from digital arts and moving into immersive work. At the other end of the spectrum, higher grants support large-scale, multi-user or interactive projects requiring substantial production means (testing, development, production, etc.).

These public subsidies rely on a principle: for every euro granted by the CNC, the producer must secure an equivalent euro from other sources—public funding (local authorities or France Télévisions through its Storylab, one of the major producers in France) or private financing. These contributions may come directly from the production company or from third-party partners injecting capital into the project. One example is Vive Arts, a division of HTC, which in recent years has co-produced experiences such as Playing With Fire (Atlas V) presented at the Philharmonie, or Versailles: Lost Gardens of the Sun King (GEDEON Experiences, Small Creative). On paper, the model appears virtuous for public authorities: each euro invested mechanically generates an additional euro in the sector. For example, if a work receives €50,000 in support, the company must secure at least an equivalent amount in private funding. In practice, this rule is more constraining for smaller production companies, which are less able to secure private or self-generated funding. “One option is to take on debt; another is to move more slowly on a project to allow time for money to come in,” explains Mathieu Pradat. “Some producers have stronger financial resources because they provide paid services for third parties. Conversely, this system disadvantages ambitious independent narrative projects that require time for editorial development. Yet these are arguably the projects most likely to engage audiences in a critical conversation about XR, much like cinema or theatre. The quality of that conversation is one of the conditions for the sector’s economic emancipation.” Producers can nonetheless apply for “fragile work” status, when distribution circuits, shooting conditions, or production constraints create excessive complexity. This exemption then allows the private funding requirement to drop to 20%. A reflection is currently underway at the CNC to make access to this exemption easier. A reflection is currently underway at the CNC to make access to this exemption easier.

Strengthening financing capacity

That said, some industry players have greater financial capacity and appear to be accelerating their structural development. As a result, they are increasingly able to self-finance part of their projects. One strategy involves internalizing XR production capabilities. Several companies have already begun this shift. This is notably the case for Atlas V and Lucid Realities, two of the companies most frequently supported by the CNC in 2025. By bringing technical and artistic expertise in-house, these producers reduce external costs and secure greater control over their operations. This approach enables them to develop projects that carry lower financial risk, while also supporting more experimental productions in parallel. As Chloé Jarry, founder of Lucid Realities, explains: “This internal team also allows us to maintain control over research and development and to preserve project quality. In a still-evolving market, retaining our expertise is essential. It also gives us the flexibility to invest our own funds in more artistically driven proposals.” Conversely, a second strategy is emerging: technical studios stepping into production roles themselves. This reflects a sector still undergoing transformation, where the boundaries between service provider and producer are becoming increasingly blurred. Backlight offers a telling example. Initially positioned as a technical studio, the company has begun developing its own projects, such as La Magie Opéra. “The development phase received preproduction support from the CNC. We looked for sponsors—like Chanel, which supported Le Bal de Paris—but that effort did not succeed. In fall 2024, we ultimately decided to move forward with a more modest scope. We have several partners, including the Vive Arts fund, along with support from the City of Paris,” explains Frédéric Lecompte, founder of Backlight. These integrated capabilities have also been enabled by new capital inflows. A few years ago, tech giants such as Meta invested heavily in immersive creation—until 2024, when the company redirected its investments toward artificial intelligence. Today, HTC VIVE appears to be the most active corporate investor in the market. The Taiwanese headset manufacturer has taken stakes in several French production companies and studios. “These investments are carried out directly by HTC group entities across different organizations. Atlas V represents the most recent investment,” explains Thomas Dexmier, General Manager of HTC VIVE Europe. The fundraising carried out in early 2026 is thus estimated at around five million euros. “The goal is to strengthen our production capacities and to establish a lasting position in these formats, which are currently experiencing the strongest growth within the VR ecosystem,” said Antoine Cayrol, co-founder of Atlas V, in Fisheye Immersive. “This fundraising will allow us to reach a new stage and amplify our strategy (…) LBVR (ed.: location-based entertainment and VR).”

While confidential negotiations do not allow the exact nature of the agreements to be disclosed, the Taiwanese company has nevertheless acquired significant stakes (estimated in the seven-figure range) in other French companies: Backlight, Lucid Realities, Small Creative as early as 2024, and Excurio well before that date.

Thomas Dexmier, Manager général HTC VIVE Europe, durant Laval Virtual 2026

International Co-productions

These accelerating structures share a common trait with smaller producers: all, largely grouped within the PXN network, are seeking to position their projects within international co-production logics. One example is Noire, one of the most exported XR works according to the 2024 Unifrance ranking, produced by Novaya with support from TAICCA (Taiwan). These co-productions have become almost a prerequisite to reach budgets compatible with XR’s artistic ambitions. To facilitate them, the Institut Français, CNC, and Unifrance launched the “French Immersion XR” program in 2023, aimed at supporting producers’ travel to major international festivals (60 trips supported in 2025 across 22 events worldwide). Several territories now stand out as major hubs of immersive production. Canada, first, via SODEC, with an envelope estimated at around €9 million over three years under its “Strategy for the Growth of Digital Creativity in Culture (2023–2028),” plus €600,000 in export support in 2025. Taiwan, via TAICCA, though funding figures remain undisclosed. And Luxembourg, where the Film Fund remains a key interlocutor for European producers, with an estimated €1.09 million dedicated to immersive projects in 2025. Other signals are emerging, notably in Germany, where new funds via FFF Bayern or Medienboard Berlin-Brandenburg have recently been announced.

Filmfund – Luxembourg City Film Festival, Pavillon VR 2024

From one country to another, funding mechanisms differ significantly, making precise comparisons difficult. Luxembourg illustrates this specificity. Unlike countries such as Belgium, where tax incentives like the Tax Shelter encourage production location, Luxembourg relies on direct and selective mechanisms. As Gwenael François, director and producer at Skill Lab, noted in XRMust: “One of Luxembourg’s specificities is the ability to finance immersive projects through the same window as cinema. This single desk really simplifies producers’ work.” In practice, immersive projects can be evaluated under rules similar to cinema, with budgets reaching up to €1.5 million. However, Film Fund Luxembourg support takes the form of repayable advances, whereas the CNC in France provides non-repayable grants. All these technical differences make comparisons difficult, sometimes even speculative. One conclusion nonetheless stands out: the CNC remains by far one of the largest direct public funding bodies for immersive creation in Europe, and likely one of the most significant globally.

Distribution: The Real Battleground

Up to this point, the analysis of production funding remains relatively clear. It becomes far more complex when considering the full value chain. In other words, looking from creation to production to distribution reveals the real circulation of financial flows. In this still-emerging industry, distribution is clearly the weak link in the economic model. For years, professionals have searched for a sustainable model. First, large-scale immersive projections found audiences through major events (Fête des Lumières in Lyon, Rencontres Audiovisuelles in Lille, Constellations in Metz) and dedicated venues such as L’Atelier des Lumières. Some investors are beginning to emerge, such as the Grand Palais Immersif in Paris, a subsidiary of RMN-Grand Palais, which opened in 2022 with Banque des Territoires (France 2030) and Vinci Immobilier, and has since opened its capital to Chargeurs Museum Studio (with Michael Fribourg) now the majority shareholder (52%). However, augmented, virtual, and mixed reality works are still rarely distributed. Digital art festivals have limited capacity, and major film festivals, despite larger audiences, rarely pay authors, considering these events to be promotional in nature (read the article published on NECTART).

Today, however, one market appears to be taking shape for these works: location-based entertainment (LBE). These multi-user experiences, anchored in dedicated venues, open up promising economic perspectives. This trend is particularly evident internationally. In Unifrance’s 2024 report, French Immersive Works Abroad and at International Festivals, China is identified as the leading country in terms of revenue generated from imported immersive works. The report also notes: “In China, the dominant model is large-scale free-roaming LBE, capable of accommodating dozens of participants simultaneously in vast environments.” Thomas Dexmier of HTC VIVE confirms this trend: “LBE offers great narrative freedom and generates extremely enthusiastic audience responses.” Through this model, companies such as Excurio have developed immersive expeditions capable of hosting up to 120 visitors at once, allowing them to explore shared virtual worlds. Each participant experiences the narrative individually while moving through the same physical space. This dynamic has been accompanied by growing interest from major cultural institutions—particularly museums—which see immersive formats as an opportunity to renew visitor experiences and diversify interpretive approaches. This direction closely aligns with the mission pursued by VIVE Arts. As Celina Yeh, executive director of the brand, explains: “VIVE Arts has collaborated with prestigious institutions such as the Victoria and Albert Museum and Somerset House in London, as well as UNESCO World Heritage sites such as the Terracotta Army in Xi’an. In France, emblematic institutions including the Musée du Louvre,the Musée d’Orsay,the Musée de l’Orangeriethe Musée d’Art moderne de Paristhe Château de Versailles, l’Opéra national de Paris and Philharmonie de Paris have developed spectacular immersive experiences with us in recent years.”

Investments by Pierre-Édouard Stérin

At the same time, the sector has recently seen the emergence of new private actors whose arrival has sparked concern among parts of the XR community, including in a December 2025 op-ed in Le Nouvel Obs. At the center is Otium Leisure, the investment company of right-wing entrepreneur Pierre-Édouard Stérin. Through this structure, major investments have been made in immersive distribution, notably via the Hadrena fund (which reportedly secured a €140 million loan from Eurazeo in 2024, indicating its financial scale), which launched Eclipso in 2022. Stérin appears to be less involved in production than in distribution, via Eclipso and also the “Cités Immersives” brand led by Jean Vergès, who, after initially benefiting from his support, is now distancing himself. This strategy reflects a clear reading of the market: economic traction lies on the distribution side.

Indeed, several French producers and studios have contributed works now exhibited in Eclipso venues. This includes Excurio, behind experiences such as Horizon of Khufu and Lost Worlds, as well as Small Creative, which notably developed Titanic: The Immersive Dream. In any case, the large-scale distribution of certain LBE works demonstrates that a degree of profitability is now achievable within the XR field. This evolution may ultimately influence the very nature of the projects being produced. In other words, could this shift reshape artistic forms themselves? The hypothesis is far from far-fetched—particularly given comments recently shared anonymously by a CNC official with HACNUMedia: “The CNC is not intended to support sectors indefinitely if they lack a viable market.” A notable exception exists in the case of short films, historically considered a laboratory for developing feature-length storytelling—something that is far from the current reality of XR.

Structural Investments

Since distribution is now central to XR, building a distribution network has become a priority for public authorities. This is one of the goals of France 2030, led by the General Secretariat for Investment, through the “Immersive Culture and Metaverse” program (estimated at €150 million) and, to a lesser extent, through “Digital Transition and AI Adoption,” whose budget has not been disclosed. This investment plan has supported numerous initiatives dedicated to XR distribution, including L’hybride in Lille (with MODULOPI), the TRAVERSE project led by Diversion with Art Explora, Futura Cinema, and HACNUM. Other audiovisual and museum actors are also involved, such as Mk2 with its Mk2 Centre des Arts project, and the Cité des sciences et de l’industrie, which plans to open an immersive room next year. Without structural support, such infrastructures would be difficult to build. As Nicolas Gendrault, head of production and development at Cité des sciences et de l’industrie : “Investment related to building and opening a venue quickly reaches the million-euro mark. Technological deployment also plays a major role: a simple VR installation requires technical infrastructure, but as soon as immersive sound is introduced, acoustic insulation and costly distribution systems become necessary. And for monumental projection, ceiling height becomes a critical factor in achieving a genuine sense of immersion.” He continues: “Even if ticket revenue is anticipated, the question of upfront investment and initial cash flow remains central. It is also difficult to attract partners or operators if venues are not already equipped and operational.” The Cité des sciences et de l’industrie nonetheless benefits from a major advantage:“We already have identified spaces and an annual attendance of nearly two million visitors. The brand image of a cultural institution plays a decisive role. Other stakeholders, particularly private ones, must invest heavily in communication to establish their legitimacy.” .”

L’Hybride à Lille

This reveals a paradox for major cultural institutions: a strategic advantage in terms of artistic projects and audience development, but financial constraints that rarely allow such investments. Ultimately, the gradual construction of a distribution network may not necessarily lead to a redistributive model like cinema’s, where part of box office revenues is reinvested into the sector. In XR, however, a key limitation appears: most works shown in France are domestically produced. In this context, taxing CNC-supported works would be counterproductive.

A Fragile Future for Immersive

France is therefore one of the XR leaders, thanks to strong public support for production and an ecosystem structured around public investment. This model is also inspiring other countries. In the Netherlands, for instance, the recent CIIIC program (around €270 million) reflects a similar ambition. This favorable context attracts new private investors. That said, it is important to keep perspective: the French XR sector remains heavily dependent on public institutions. Without this policy, much of the ecosystem described here would simply not exist.

Two conclusions emerge. The first concerns economic sustainability: in the medium term, the sector will need to stabilize a viable economic model. Public investment cannot remain unlimited without market returns. The second concerns the central role of the CNC in this fragile balance. The institution remains at the heart of XR funding, and its future will depend in part on its ability to preserve its resources in an uncertain political context. As Gaëtan Bruel noted in Le Film français: “Weakening the CNC’s resources means organizing a cultural and industrial decoupling,” including in XR. Regularly challenged by the far right, the CNC could face broader instability ahead of the 2027 presidential election. The popular saying goes that business and politics should not mix… really?

For the past decade, Adrien Cornelissen has explored the frictions between technology, contemporary creation, and the cultural and creative industries. A journalist and ideas curator, he contributes to publications such as Fisheye Immersive, XRMust, Nectart, and the Revue AS. He also leads the development and editorial coordination of HACNUMedia, a media platform focused on technological shifts in the arts and culture sector. As a speaker at festivals and higher education institutions, he also advises cultural organizations and artists through his agency Bas·alt.